Tendering vs Negotiation

Price Expectation and Final Cost in High-End Residential Construction

An evidence-based review for private residential clients in the UK

Alex Beaugeard

Director, Multipli Consulting

Nick Walton

Director, Walton Wagner

Jay Hodges MRICS

Construction Director, Remian Group

Jakob Mayer

Project Manager, F/LIST

O V E R V I E W

Executive Summary

This report examines the gap between price expectations at the point of engagement and the price ultimately paid at project completion, contrasting competitive tendering with negotiated procurement in the context of high-end residential construction in the United Kingdom. It brings together quantitative industry evidence and direct practitioner experience from over two decades of delivering prime residential projects.

The evidence consistently points in one direction: competitive tendering produces an artificially low initial price that bears little relationship to what a client ultimately pays. Negotiated procurement produces a higher but more honest opening figure that remains far closer to the final account.

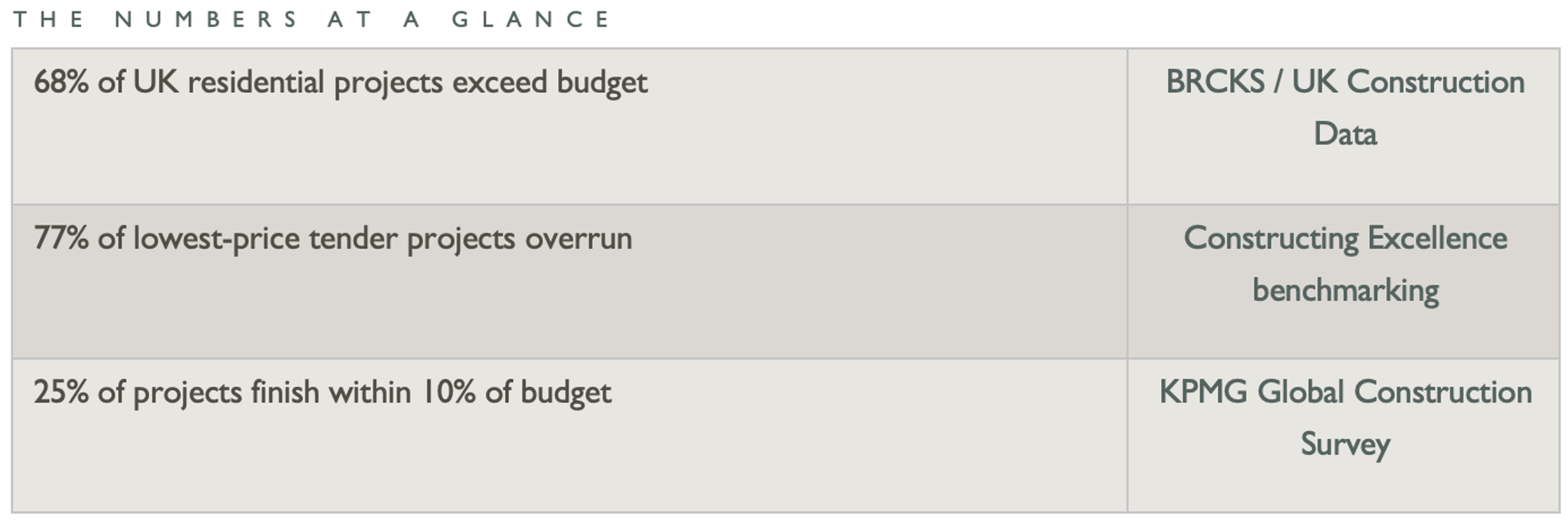

ⓘ Sources: BRCKS UK Construction Data; Constructing Excellence KPI Report; KPMG Global Construction Survey

“The central finding: in competitive tendering, clients are frequently presented with a price that is structurally designed to win the contract, not to reflect the true cost of delivery. The gap between that opening number and the final account is where the real cost of tendering is hidden.”

- Multipli, May 2026

Four headline conclusions emerge from the research and practitioner evidence:

Competitive tender prices are routinely artificially suppressed at point of engagement, with contractors pricing to win rather than to deliver, recovering margin through variations, claims and programme extensions during the build.

Negotiated contracts produce far greater cost certainty from the first figure to the final account. Academic case study evidence from UK construction shows negotiated final accounts can land as close as 1.3% above the original contract sum.

A hybrid route, competitive tendering for enabling and structural works, negotiated procurement for fit-out and interiors, is emerging as a successful adaptation for complex prime residential projects.

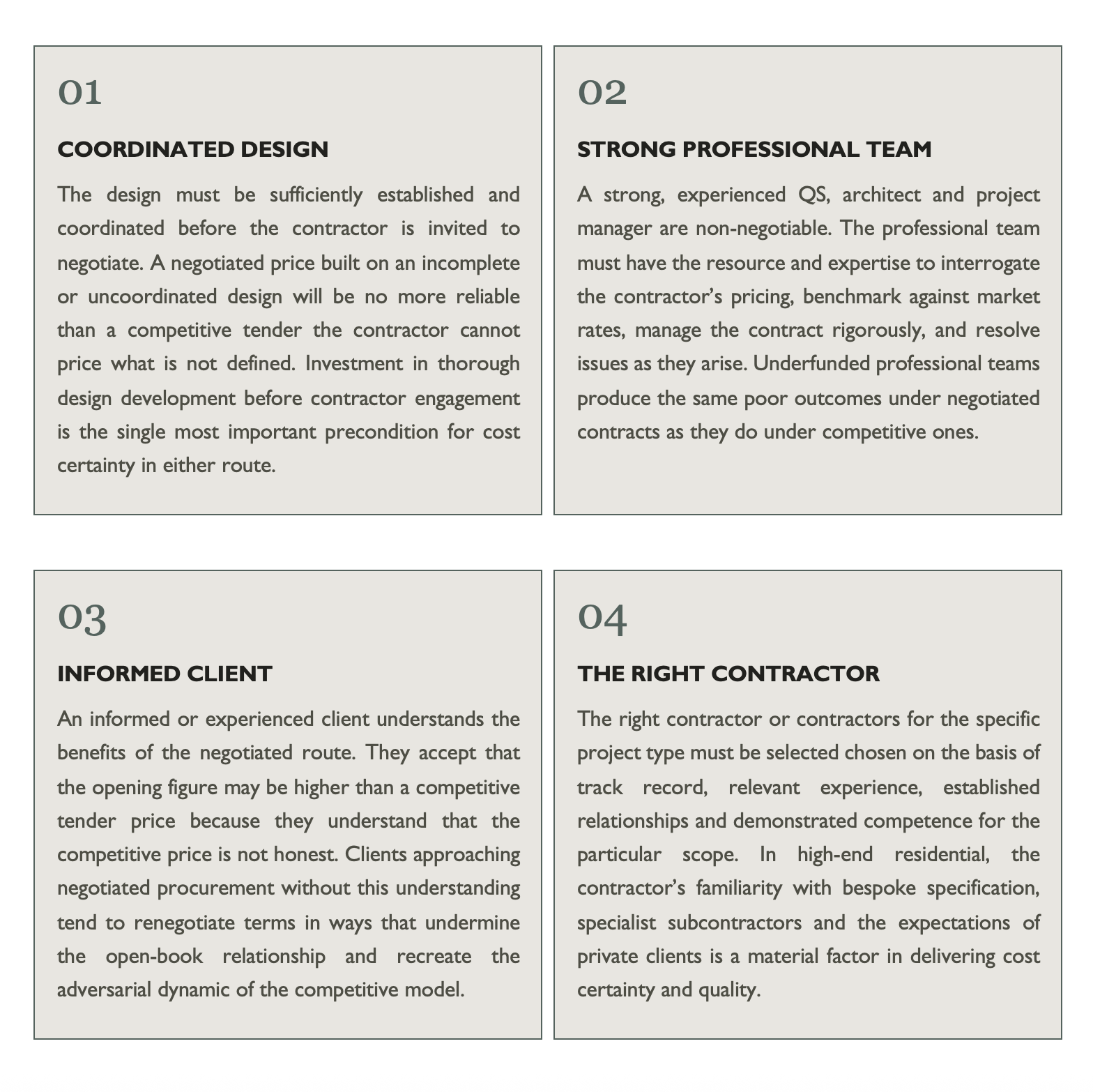

Success in negotiated procurement depends on four conditions: a coordinated design, a strong professional team, an informed client, and the right contractor selected for the specific project type.

E V I D E N C E

1. The Scale of the Problem

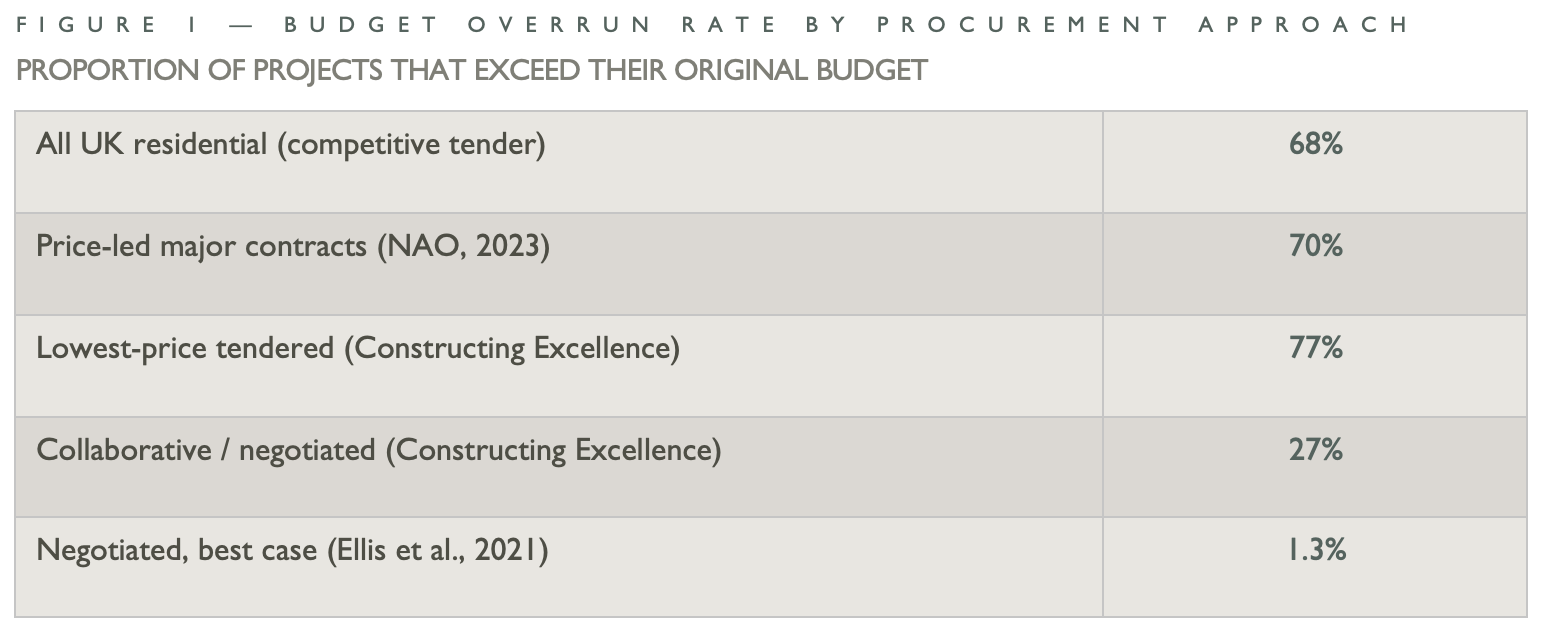

Before examining the two procurement routes in detail, it is important to establish the scale of the cost overrun problem in UK construction. The data is striking.

ⓘ Sources: BRCKS UK residential data; NAO 2023; Constructing Excellence benchmarking; Ellis et al. (2021) Buildings 11(6)

The Constructing Excellence comparison is particularly instructive: projects procured through collaborative or negotiated frameworks overran at a rate of 27% versus 77% for lowest-price tendered projects, a threefold difference in the probability of a client paying more than they expected.

McKinsey Global Institute research across 900 major projects found that the average cost overrun across the construction industry sits at 28–33% above initial estimate. KPMG’s global construction survey found that only 25% of projects finish within 10% of their budget. These figures are not aberrations: they are the structural outcome of a procurement model in which the opening price is not designed to be accurate.

For UK residential projects specifically, BRCKS data indicates 68% of projects exceed their budget, with an average overrun of £23,000 on a typical residential contract. On high-end projects, where contract values are an order of magnitude higher, the absolute figures are proportionally larger.

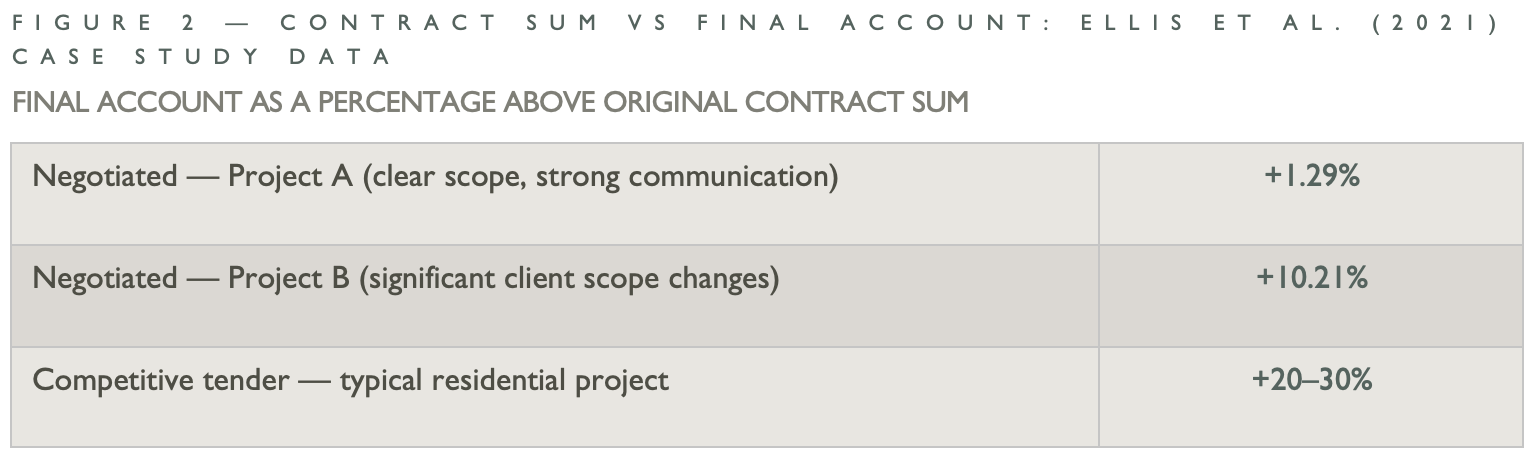

ⓘ Source: Ellis et al. (2021). A Case Study of a Negotiated Tender within a Small-to-Medium Construction Contractor. Buildings 11(6), MDPI.

The Ellis et al. data is the most robust UK-specific quantitative evidence available on negotiated tender cost performance. Project A, where the scope was clearly defined and communication was strong, came in at just 1.29% above the contract sum. Project B’s 10.21% variance was driven 51.28% by client-initiated scope changes, not by contractor under-pricing or cost recovery: a fundamentally different, and more manageable origin for cost growth.

A N A L Y S I S

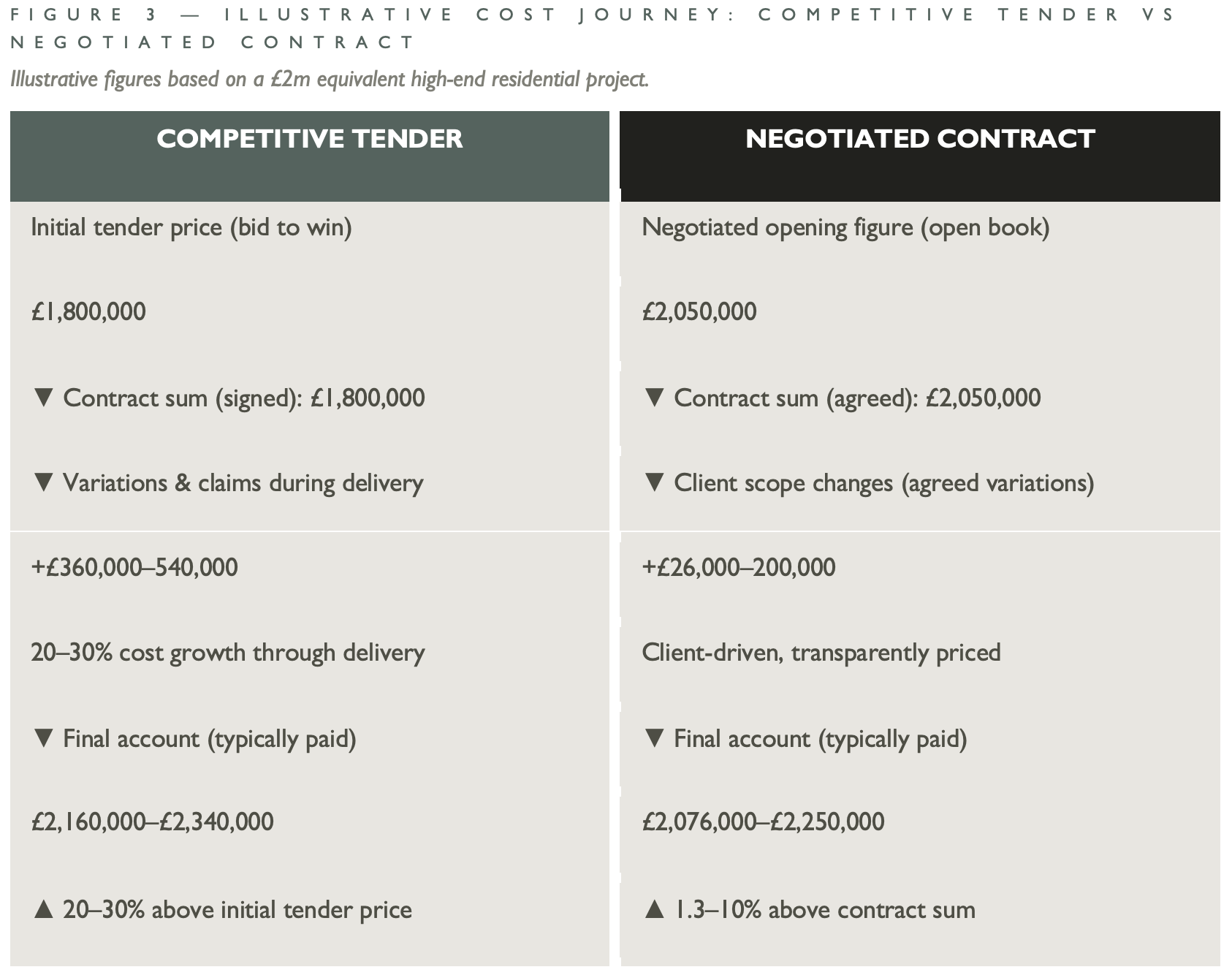

2. The Cost Journey

The most important question for a private residential client is not ‘what is the tender price?’ but ‘what will I actually pay?’ The two procurement routes produce very different journeys from initial figure to final account.

ⓘ Illustrative projections derived from: Constructing Excellence (2011); Ellis et al. (2021); Planman UK architects’ cost overrun data (2024); NAO Major Projects Authority data (2023).

The critical observation in Figure 3 is not just the size of the final figure but its origin. Under competitive tendering, cost growth during delivery is largely driven by the contractor recovering margin through variations and claims on works that were always in scope but never honestly priced at tender. Under negotiated procurement, the cost growth that does occur is predominantly the result of the client’s own decisions to extend or enhance the brief, a very different, and much more controllable, type of expenditure.

This distinction is particularly material in high-end residential where the brief is heavily weighted towards interior design and specification. As Nick Walton, Director of Walton Wagner, observes from direct practice: a negotiated contract allows the client to change or develop their brief without being penalised by a contractor looking to claw back costs from a lowest-price award. That flexibility, within a framework of honest pricing, is one of the principal financial advantages of the negotiated route.

A N A L Y S I S

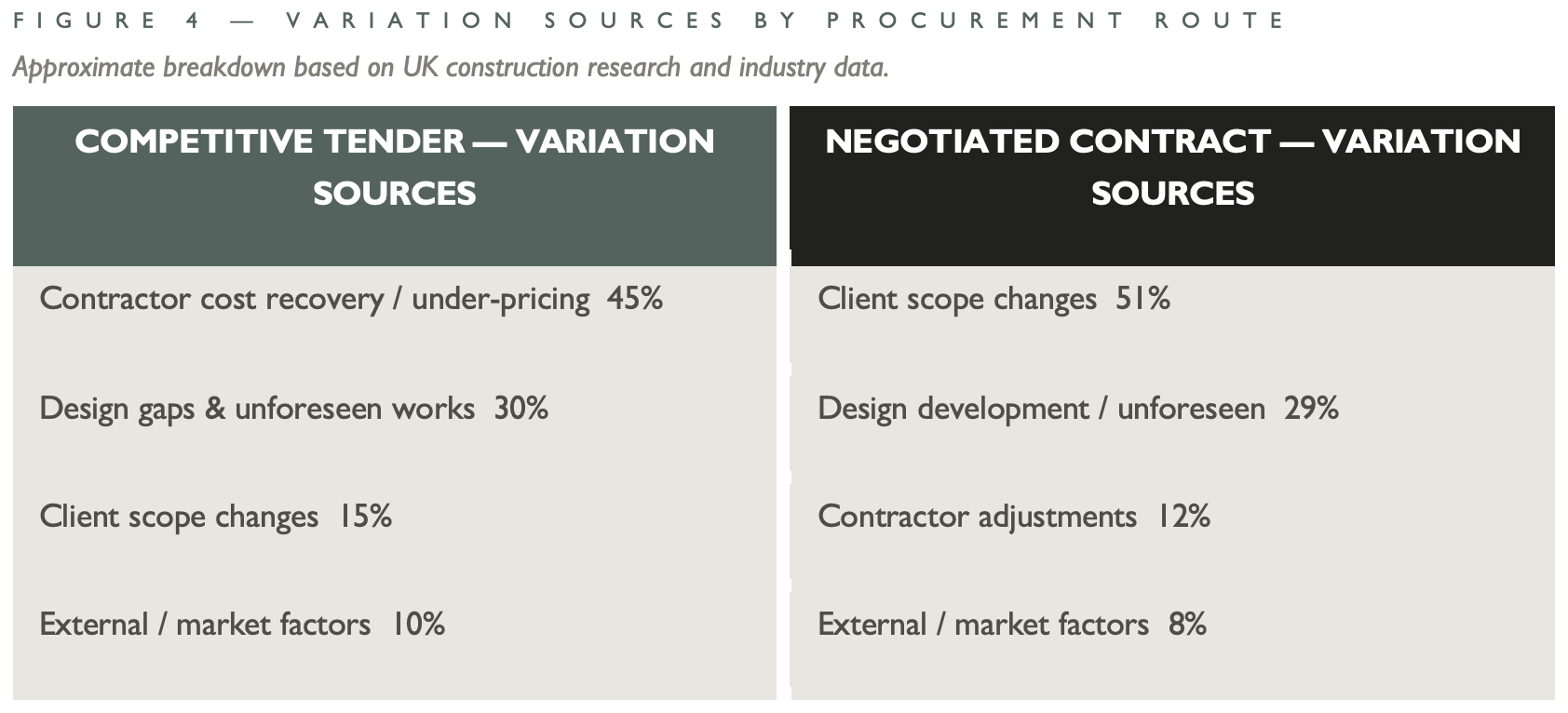

3. Where Do Variations Come From?

Understanding why costs grow is as important as understanding that they do. The origin of variations differs substantially between the two procurement routes, and this difference matters enormously for a client’s ability to plan and control their budget.

ⓘ Competitive tender variation sources: synthesised from Constructing Excellence (2011); Designing Buildings Wiki; Planman (2024). Negotiated variation sources: Ellis et al. (2021) — client-driven 51.28% figure is directly measured.

Under competitive tendering, the largest single driver of cost growth is contractor under-pricing and cost recovery, works that were within the original scope but priced at insufficient rates in order to win the contract, and subsequently claimed as variations or uplifts during delivery. This is a structural feature of the competitive tender model, not an anomaly.

Under negotiated procurement, Ellis et al.’s case study provides a precisely measured figure: 51.28% of all project variations were directly initiated by the client changing or extending the brief. This is not a cost overrun in the conventional sense; it is a client choosing to spend more. The remaining variations were transparently priced and agreed in advance rather than emerging as contested claims at the end of the project.

H I S T O R I C A L C O N T E X T

4. How Did We Get Here?

Understanding the current state of procurement in high-end residential requires a brief look at the conditions that produced it. The dominance of competitive tendering and its attendant problems did not emerge by accident, it was the product of specific structural pressures applied to the industry over several decades.

The 45% cost-recovery figure represents something contractors know from inside the process. Under traditional competitive tendering, the lowest-price mechanism rewards the most aggressive pricing regardless of intent. Across many bids over time, it selects for the bid that least resembles the eventual cost of delivery. Recovery is then sought through the only mechanisms available, variations against incomplete scope, claims against ambiguous specification, programme extensions against compressed preliminaries.

“The 45% figure is the visible footprint of an entirely predictable process. The lowest-price mechanism rewards the most aggressive pricing — and recovery is then sought through the only mechanisms available. This is not a moral failing of contractors. It is a rational response to a procurement structure that allows for it.”

— Jay Hodges MRICS, Construction Director, Remian Group

“Historically the race to the bottom approach, incomplete design and using Design & Build procurement in high-end and prime residential, has been a major risk and a cause of cost and programme uplift.”

— Nick Walton, Director, Walton Wagner

Funders without construction experience

For much of the modern development cycle, project funding has been defined by funders and bankers with no direct construction experience. For those parties, cheapest was best, and so competitive tendering, with its superficially attractive opening numbers, became the default. The true cost of that approach only became apparent once the project was under way and variations began to accumulate.

Design & Build in the wrong context

Design and Build procurement, in which the contractor takes responsibility for both design development and construction, has been widely used in the residential market. In standard housing, this is a reasonable model. In high-end and prime residential, where specification is bespoke and the client’s involvement in design decisions is continuous, it creates significant risk: the contractor’s financial interest in compressing specification conflicts directly with the client’s interest in refining and enhancing it.

Clients are underinvesting in design development

A recurring cause of cost growth across both procurement routes is the appointment of a contractor before the design is sufficiently developed. When a contractor, whether tendering or negotiating, is asked to price from incomplete information, they must either price conservatively (and appear expensive) or price optimistically (and recover costs later). The client who invests in thorough design development before contractor engagement removes this ambiguity and materially improves their ability to get an accurate price under either route.

Underfunded professional teams

The trend toward lower professional fees applied to architects, quantity surveyors and project managers has had a direct impact on the quality of project oversight. A professional team resourced at below-market rates cannot deliver the level of design coordination, cost management and contract administration that a complex high-end residential project demands. The resulting gaps in scope definition and cost control create exactly the conditions in which competitive tender overruns flourish.

“The trend to pay small fees for the professional team led to poor resource allocation to match the fee. A strong and experienced QS, architect and project manager are fundamental prerequisites for the negotiated route to succeed.”

— Nick Walton, Director, Walton Wagner

“The procurement shifts this paper advocates is not an accusation of anyone. It is an invitation. The negotiated and CM/MC routes work because they rebuild the conditions in which the original interests of clients, professional teams and contractors are aligned rather than structurally opposed. For contractors, that means delivering rather than recovering — which is what most of us came into the industry to do.”

— Jay Hodges MRICS, Construction Director, Remian Group

S U M M A R Y

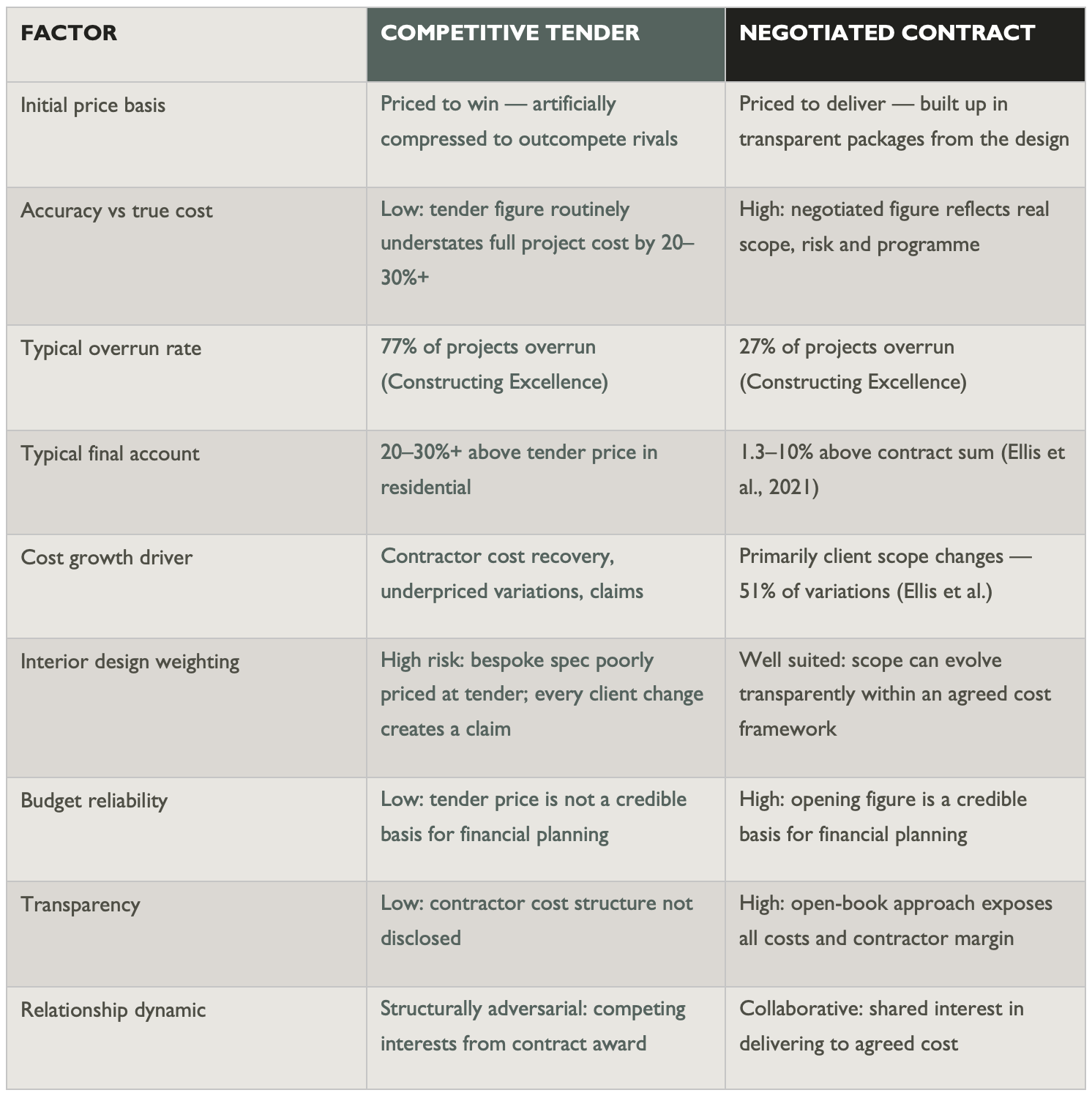

5. Side-by-Side Comparison

The table below summarises the key differences between the two procurement routes as they relate to price expectation and final cost in UK high-end residential construction.

P R A C T I T I O N E R G U I D A N C E

6. Prerequisites for Success

Negotiated procurement is not a panacea. Its advantages cost certainty, transparency, collaborative delivery only materialises when the right conditions are in place. Based on direct experience across prime residential projects, Nick Walton of Walton Wagner identifies four conditions that are essential to a successful negotiated outcome.

Overcoming the ‘ripped off’ concern

Even clients who intellectually accept the case for negotiated procurement often retain an instinctive concern: without competitive comparison, how do they know they are paying the right price? This is a legitimate question, and the answer is not to abandon cost scrutiny it is to apply it more intelligently.

“Clients still need to feel or see they are paying the right price and overcome the fear of being ‘ripped off by the builder’. Still competitively tender the fixed costs of delivery this helps the open-book and transparent process during construction.”

— Nick Walton, Director, Walton Wagner

Selectively tendering the fixed, measurable costs of delivery preliminaries, scaffolding, plant, waste disposal provides a market reference point that supports the open-book process and gives the client confidence that the contractor’s costs are reasonable. This is not a return to competitive tendering for the whole project; it is a targeted application of competitive discipline in the areas where it genuinely works, combined with the transparency of negotiation in the areas where it does not.

From the contractor's side of the table, the four prerequisites read as four enablers of honest delivery. A coordinated design allows the contractor to price the building rather than assume it. A capable QS testing the numbers monthly is not a gatekeeper against the contractor. It is the validation mechanism that makes an open-book commitment commercially credible.

“We actively recommend that every client appoints an independent QS to test our pricing throughout the project. Transparency is most credible when verified by someone with no commercial relationship to the contractor. We would rather a capable QS tested our pricing than ask a client to trust it.”

— Jay Hodges MRICS, Construction Director, Remian Group

INNOVATION

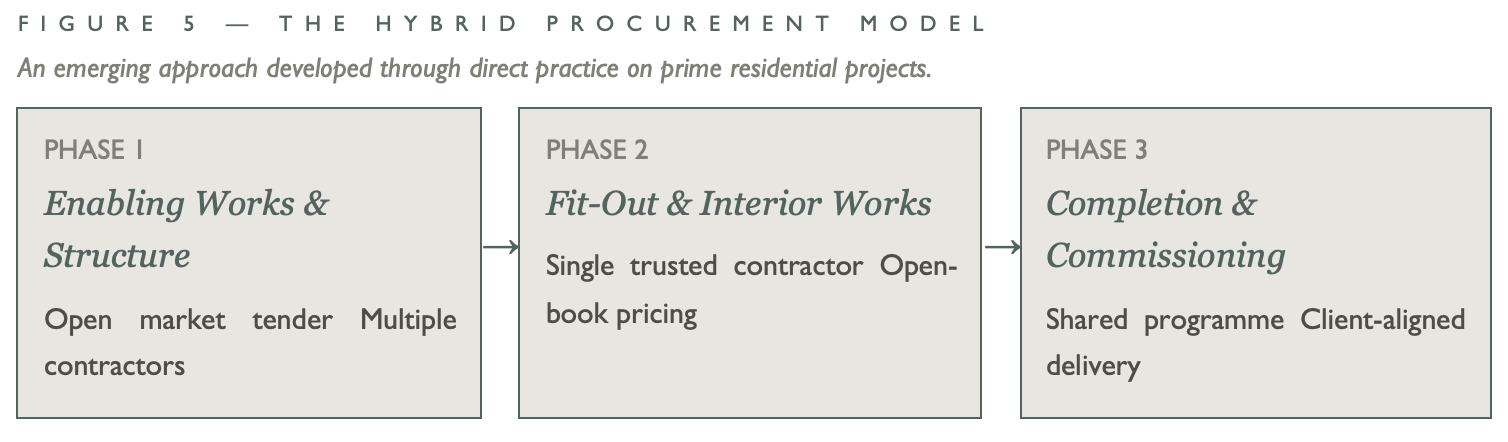

7. The Hybrid Route

Emerging practice in prime residential construction points to a third way a hybrid procurement model that applies the right approach at the right phase of the project. This is not the traditional two-stage tender, but a distinct adaptation developed through experience on complex high-end schemes.

“As a hybrid approach, we are seeing a split procurement route: competitive tendering for the enabling and structural works on the front end, and then a more negotiated approach for the fit-out. This has been successfully completed. It is not the old two-stage procurement route but an adaptation of it.”

— Nick Walton, Director, Walton Wagner

Why the split works

The logic behind the hybrid model is straightforward. Enabling works and structural frames — substructure, superstructure, concrete, steelwork are relatively well-defined scopes that can be priced accurately from engineering drawings. Competitive tendering is a reasonable approach for these elements: the scope is measurable, the risks are known, and the market for this type of work is deep and active.

Fit-out and interior works are fundamentally different. The specification is bespoke. The brief evolves as the client makes decisions about finishes, technology, joinery and furnishings. The number of specialist subcontractors with the relevant expertise is limited. In this environment, competitive tendering produces exactly the problems described elsewhere in this report: artificially low prices, poor scope definition, and adversarial delivery. Negotiated procurement, applied at this phase, resolves all of these.

The hybrid model, therefore, extracts the genuine efficiency benefits of competitive tendering, where they exist, while applying the superior cost certainty and collaborative delivery of negotiated procurement, where it is needed most. For large and complex prime residential projects, this may represent the most sophisticated and commercially intelligent procurement approach currently available in the UK market.

The hybrid procurement model matches how Remian increasingly works on complex prime residential schemes. Substructure, superstructure and primary envelope can be measured and priced competitively. Fit-out is fundamentally different: bespoke specification, an evolving brief, and a limited pool of specialist trades capable of the work. The key risk in splitting procurement is at the join, and clients who think carefully about interface protocols and accountability at that boundary are better served by the model than those who treat procurement as the only decision.

“The logic of split procurement, from the build side, is intuitive once you stop treating procurement as a single decision that must apply to every package on the project. The structural work can be tendered. The fit-out cannot be done honestly that way.”

— Jay Hodges MRICS, Construction Director, Remian Group

C O N T E X T

8. Why This Matters More in High-End Residential

The dynamics described throughout this report apply across construction generally, but they are amplified in high-end residential work for several specific reasons.

Specification complexity

High-end residential projects involve a density of bespoke specification specialist stone, custom joinery, integrated technology, heritage materials, and architectural metalwork that is inherently difficult to price accurately from drawings alone. A competitive tender price for this work is, at best, an informed estimate and, at worst, a placeholder that will be renegotiated during the build.

Interior design weighting

Projects that are heavily weighted towards interior design, where the value is primarily in finishes, furnishings and craftsmanship rather than structure, are particularly ill-served by competitive tendering. The specification for this work is inherently evolving as the client makes design decisions, and a contractor who has won on the lowest price has every incentive to treat every design decision as a variation claim. Negotiated procurement, by contrast, creates a framework within which the brief can develop without financial penalty.

Design evolution

Private residential clients, particularly at the upper end of the market, expect to continue refining their brief during the build. A competitive tender locks the contract sum against a specification that may be only partially resolved; every client change becomes a variation, and an opportunity for cost recovery. A negotiated contract accommodates design evolution with agreed mechanisms for transparently pricing changes at market rates with known margin.

Programme risk

In high-end residential, programme overruns are disproportionately costly, both financially (financing costs, rental costs for displaced residents) and personally. Competitive tendering, by compressing preliminaries and programme contingency at bid stage, creates the conditions for exactly the slippage clients most want to avoid. A negotiated contractor who has set the programme with full knowledge of the scope produces a more reliable completion date.

The relationship premium

At the upper end of the residential market, the quality of the client-contractor relationship is itself a material consideration. Projects of significant personal importance a family home, a long-planned renovation are not served by a procurement route that places contractor and client in structurally opposing positions from contract award. Negotiated procurement, selecting a contractor on merit and engaging them as a collaborative partner, creates the conditions for a fundamentally different working relationship.

“Bespoke specification is not just difficult to price from drawings. It is impossible to price honestly — or to confirm as buildable and coordinated without specialist trade input that the conventional tender process does not have a place for. By the time the competitive tender is issued, the specialists who could have flagged the interface issues have not yet been asked.”

— Jay Hodges MRICS, Construction Director, Remian Group

R O U N D T A B L E

9. The Practitioners’ Perspective — Risk, Trust, and the Case for Open-Book

The earlier chapters establish the financial case for negotiated procurement through quantitative evidence. What the data cannot fully capture is the practitioner reality: the accumulated friction, eroded trust, and misaligned incentives that define how most high-end residential projects are actually delivered. The perspectives in this chapter draw from a roundtable discussion between Nick Walton (Director, Walton Wagner), Jay Hodges MRICS (Construction Director, Remian Group), and Alex Beaugeard (Multipli) practitioners with direct experience across design, construction management, and project delivery on prime residential schemes. Their conclusions are consistent: the problems with competitive tendering are not primarily financial but relational, and the solution requires a shift in how projects are governed, not merely how they are priced.

Risk as a manufactured problem

In the conventional procurement model, risk is treated as something to be priced and transferred. Main contractors receive it from clients; subcontractors receive it from main contractors. The result is a cascade of defensive pricing at every level of the supply chain not because the risks are inherently unmanageable, but because each party is pricing for the possibility that they alone will bear the consequences of someone else’s decisions.

Early contractor and supply chain involvement breaks this cycle. When buildability, cost, and programme are reviewed collaboratively before contracts are signed, the provisional sums and contingency allowances that generate defensive pricing are progressively eliminated. The risks do not disappear, but they become shared problems with shared solutions rather than penalties waiting to be transferred.

Open-book pricing and the OHP conversation

The most consistent point of friction in moving toward collaborative procurement is the declaration of margins. The conventional model obscures cost structure at every level; the open-book model requires that it be made visible. In practice, this means the main contractor declaring a fixed overhead and profit rate (OHP) for the project, typically around 10%, agreed upfront and held constant throughout delivery.

It is important to understand what that 10% represents. OHP covers business overheads, staff, premises, insurances, and corporate costs. The actual profit within that figure is typically closer to 2%. Making this distinction visible removes the opaque margin-recovery dynamic that drives adversarial behaviour in competitive tendering. Competitive tension is not sacrificed: individual work packages can still be competitively sourced across the supply chain, with the main contractor’s position fixed and declared. The discipline of the market is retained where it genuinely works; the hidden recovery is not.

“There is a degree of British discomfort with openly declaring margins that creates a structural obstacle to the transparency that open book requires. Addressing it requires deliberate process design, and clients who understand what they are asking for when they ask for transparency.”

— Jay Hodges MRICS, Construction Director, Remian Group

Front-end investment: buying time to save money

One of the most consistent findings from high-end residential practice is the cost of starting on-site too early. Clients often equate visible construction activity with progress, the instinct to see a shovel in the ground that pushes teams to mobilise before the design is ready. The consequences are predictable: compressed delivery windows, late design changes, and risk transfer to subcontractors at the moment of greatest damage to quality and cost.

The counterintuitive finding from practitioners is that investing more time and resources in pre-construction coordination, in design resolution, and in supply chain engagement consistently produces shorter, more efficient, and less adversarial construction phases. The upfront time cost is recovered in delivery. Before a single price is considered, competitive procurement also imposes significant administrative and compliance costs on all parties. Early engagement models, with fixed coordination fees and structured pre-construction packages, reduce this overhead materially.

Client education is a prerequisite for this approach. A client who understands that longer pre-construction means faster, cheaper, and better-coordinated delivery is a fundamentally different client to manage than one who reads an extended pre-construction programme as delay. The professional team’s role includes building that understanding from first engagement.

Design coordination: a single source of truth

A recurring failure mode in high-end residential is the disconnect between the interior designer’s aspirational concept and the physical constraints of the building. Concepts developed without early coordination with structural engineers, MEP consultants, and specialist contractors create friction when constraints emerge during construction generating costly redesign or forcing compromises that erode the client’s confidence in the team.

The response emerging from practice is a centralised model: a single, integrated source of design information combining architectural plans, BIM coordination, interiors data, structural constraints, MEP routes, material specifications, quantities, and cost data maintained collaboratively across the project team from an early stage. This is a governance approach, not a particular software platform. Within it, design review workshops replace iterative offline correspondence. Clashes are identified and resolved in real time, with all parties present. The language shifts from “value engineering”, which clients correctly perceive as cost-cutting to “design optimisation”: achieving the same aesthetic outcome through better-coordinated, better-specified means.

Specialist contractors, particularly joiners who carry significant technical design risk under current arrangements, are drawn into the process earlier and take ownership of technical drawings they already bear responsibility for. This reduces drawing volumes at sign-off stages, shortens approval cycles, and produces details that can actually be built. Architects and engineers retain guardianship of design intent; contractors take responsibility for coordination and clash resolution.

The supply chain: breaking the risk-transfer cycle

The consequences of historic risk transfer are visible in how subcontractors price work. Years of race-to-the-bottom tendering have conditioned the supply chain to assume that competitive bids are followed by change recovery. Defensive pricing and inflated provisional sums are not character flaws — they are rational responses to a procurement model that has repeatedly rewarded them.

“Defensive pricing and inflated provisional sums are not character flaws. They are rational responses to a procurement model that has repeatedly rewarded them. Change the model and the behaviour follows.”

— Jay Hodges MRICS, Construction Director, Remian Group

Early supply chain coordination changes the calculus. When specialist subcontractors are involved before designs are finalised, contributing to buildability, proposing alternatives, and identifying constraints, their relationship to the project is fundamentally different from that of a bidder responding to a tender pack. They are pricing work they have helped to define. Trust-based, long-term relationships between main contractors and key specialist subcontractors can absorb programme risk that would otherwise be defensively priced. This is not altruism; it is a rational response to the shared value created by reliable, repeat collaboration.

The valuation of off-site manufactured elements deserves specific attention. Traditional valuation practices are designed around visible on-site progress; they systematically undervalue prefabricated and workshop-built elements that represent significant real expenditure before they arrive on site. Procurement frameworks for high-end residential need to accommodate the cashflow realities of specialist manufacturers if those supply chain relationships are to be sustained.

Contracts, roles, and the reform agenda

The contract framework that governs most UK high-end residential construction typically JCT-based with extensive client-side amendments is increasingly misaligned with the collaborative delivery model that practice is moving toward. Current amendments tend to transfer design risk from professional teams onto contractors, even on fully designed projects. This produces duplicated cost for clients, inefficient contract administration, and role confusion that compounds at the subcontractor level.

The reform direction emerging from practitioner experience is clear: contractors should build; professional teams should retain responsibility for design deliverables. Contractor’s Design Portion (CDP) clauses, which push design and coordination responsibility onto contractors during execution, do not improve the programme. They defer problems rather than resolve them, and force redesign under precisely the time pressure that is most damaging to quality and cost.

Aggressive legal amendments that exceed the underlying risk’s requirements create compliance overhead without commensurate protection. A collaborative, practical review of contract terms involving all parties’ contractors, professional teams, and clients produces documents that reflect the actual allocation of risk more accurately and more fairly. The question is not which party holds the most risk; it is which party is best placed to manage each specific risk and price it accordingly.

“The question is not which party holds the most risk. It is which party is best placed to manage each specific risk. Allocate it correctly and price it accordingly — that is the basis of a fair contract.”

— Jay Hodges MRICS, Construction Director, Remian Group

O U T L O O K

10. Optimizing Project Value through Integrated Frameworks

The evidence-based comparison between competitive tendering and negotiated procurement suggests that true cost certainty is a product of trust, early information exchange, and risk transparency rather than market pressure. However, the negotiated contract should be viewed not as a final destination, but as a foundational step toward more sophisticated, collaborative frameworks. In the ultra-high-end segment, the limitations of traditional, linear procurement are becoming increasingly apparent as project ambitions begin to outpace conventional delivery methods.

“The negotiated contract is not a final destination. It is a foundational step toward something more sophisticated frameworks where all key partners share a single project culture, a single budget, and a single definition of success.”

— Jakob Mayer, Project Manager, F/LIST

The evolution toward practical necessity

What was once a visionary theory is now becoming a practical necessity for success in high-stakes construction. As the “complexity gap” widens, modern projects involve technical and logistical challenges that can no longer be solved within isolated planning silos. Research from Stanford University (CIFE) corroborates this shift, identifying integrated frameworks as the primary driver for overcoming fragmented productivity barriers. The institutionalisation of these models, now reflected in official guidelines from the German Federal Ministry (BMWSB), signals that integrated structures have become the essential operational standard for complex projects.

Evidence-based efficiency

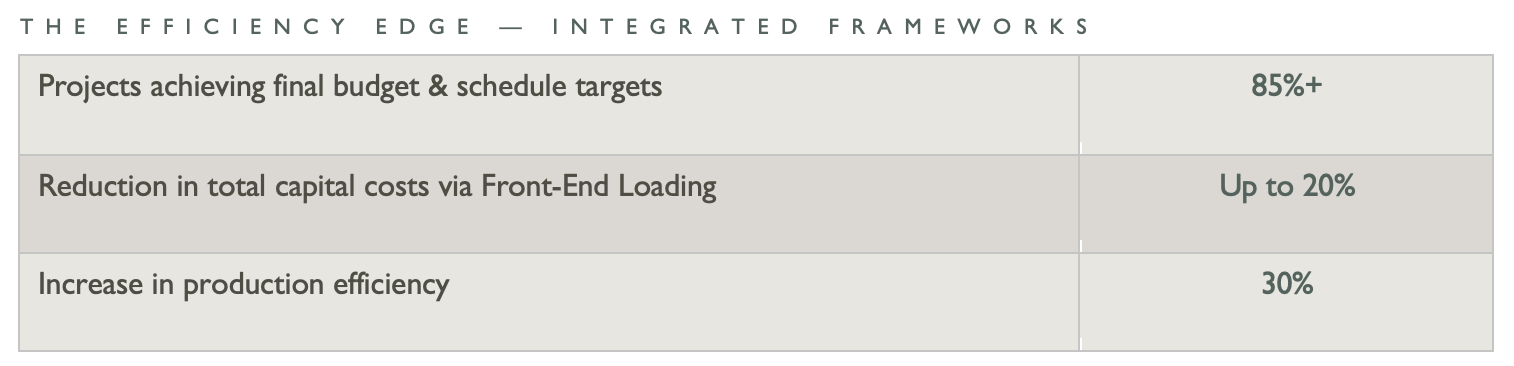

The move toward integration is an empirically driven strategic shift. It provides a striking contrast to the 77% overrun risk characteristic of traditional lowest-price tenders. Comprehensive studies show that over 85% of projects using integrated frameworks achieve their final budget and schedule commitments a direct result of a collaborative phase where risks are identified and mitigated long before the final price is locked.

Data from the McKinsey Global Institute indicates that “Front-End Loading” the practice of integrating execution expertise at the earliest conceptual stage can reduce total capital costs by up to 20%. This is achieved by resolving technical conflicts during the design phase rather than during costly on-site execution. Research confirms that integrated models lead to a 30% increase in production efficiency, eliminating the friction points of traditional, siloed procurement.

ⓘ Sources: University of Minnesota / LCI; McKinsey Global Institute; Stanford CIFE Research

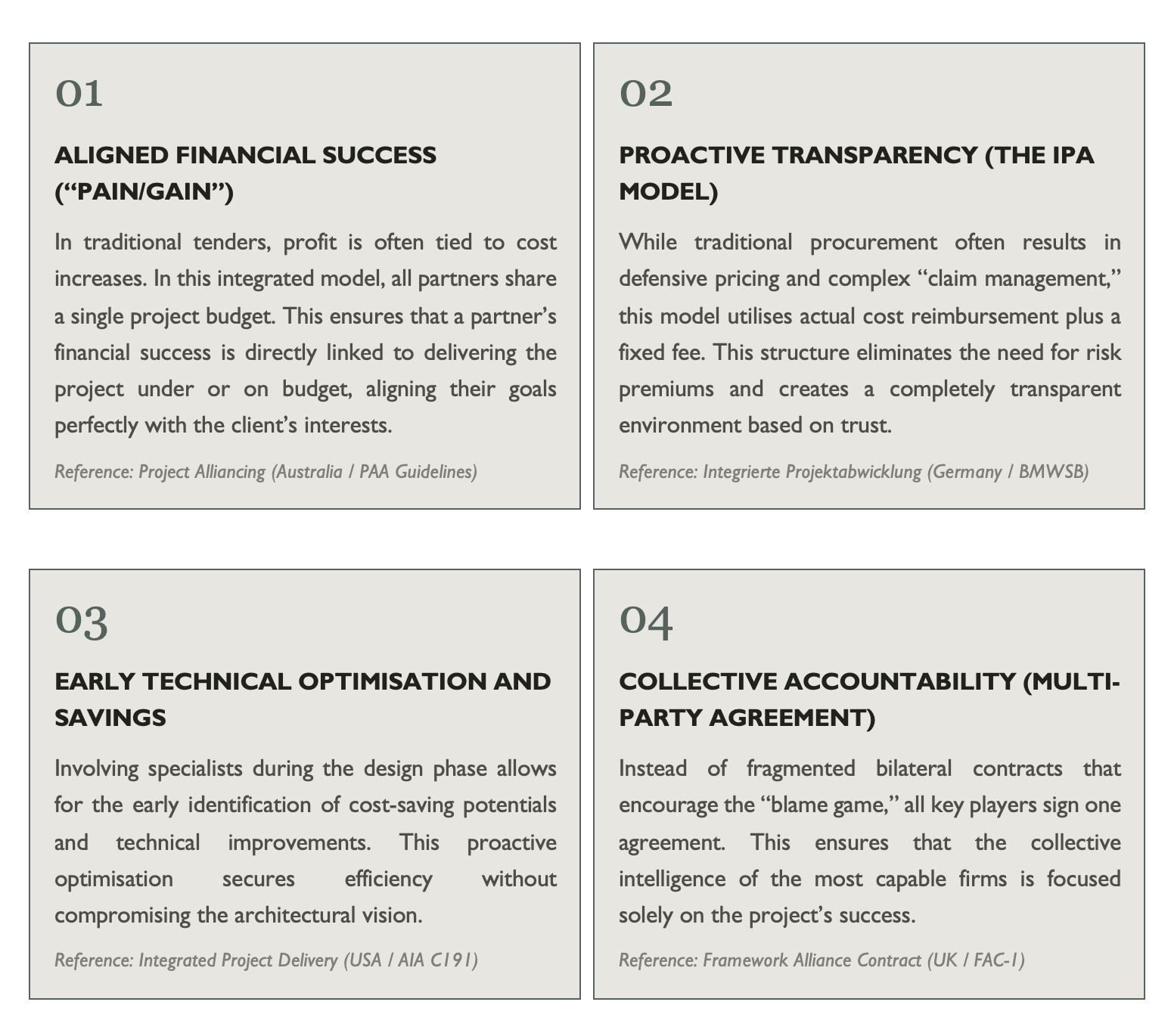

To move beyond simple negotiation, it may help to learn from global standards that have successfully resolved the “client vs. contractor” conflict, albeit in a different project style. These models provide a framework to replace the adversarial nature of traditional contracting with a unified project culture built on four core principles:

By evolving the negotiated model into these integrated frameworks, the structural inefficiencies of the traditional market are replaced by collective accountability ensuring total alignment with the client’s objectives and providing the most robust defence against the financial risks of high-end construction.

C O N C L U S I O N

11. Conclusion

The evidence presented in this report, combined with direct practitioner experience from Walton Wagner, leads to a clear conclusion: the procurement route that appears cheaper at the point of engagement competitive tendering is frequently the more expensive route by the time the project is complete. The data shows this is not a marginal or occasional difference. It is a structural feature of the competitive tender model.

Key quantitative findings from the evidence base:

77% of lowest-price tendered projects overrun their budget vs 27% of collaboratively procured projects a threefold difference (Constructing Excellence).

68% of UK residential construction projects exceed their budget (BRCKS / UK construction data).

Only 25% of construction projects finish within 10% of their budget (KPMG global survey).

Negotiated projects in Ellis et al.’s UK case study achieved final accounts of just 1.29% and 10.21% above contract sum compared to 20–30%+ typical of competitive tender residential projects.

51% of variations on negotiated projects were directly client-initiated scope changes, not contractor cost recovery (Ellis et al., 2021).

From a practitioner perspective, the negotiated route’s advantages are most pronounced in interior design-weighted projects, where the client’s evolving brief demands a procurement framework that accommodates change without financial punishment. The hybrid model, competitive for structural works, negotiated for fit-out, offers a sophisticated synthesis that applies the right tool to each phase.

None of this suggests that the negotiated route is risk-free or universally superior. Its success depends on a coordinated design, a capable professional team, an informed client, and the right contractor. Where those conditions are in place, the evidence strongly suggests it delivers a better outcome, both financially and in terms of the working relationship, than any competitive alternative.

Ultimately, this shift toward negotiation represents the first step toward a more integrated project environment. By embracing technical optimisation and collective accountability, we move beyond the friction of adversarial contracts toward a collaborative partnership, one that ensures architectural vision and financial certainty are aligned from day one.

From the contractor’s perspective, competitive tendering on the lowest price gives the client a number, but rarely the number they end up paying. The gap gets filled in across the project through variations, claims, and time. The alternative is not asking contractors to behave better. It is moving to a model where there is nothing to recover, because nothing was hidden.

“Underneath the procurement question, this paper is about something more fundamental the us-and-them mentality that has defined UK construction for decades. The negotiated route works because it removes the conditions that produce that dynamic. Contractor, design team and client are in the same room throughout. Decisions are made together because the commercial structure rewards it.”

— Jay Hodges MRICS, Construction Director, Remian Group

“The price a competitive tender presents is a bid, not a budget. The price a negotiated contractor presents is a commitment. For clients who want to know what they will pay not just what they are promised the case for negotiated procurement in high-end residential work is compelling.”

— Alex Beaugeard, Multipli

Alex Beaugeard

Multipli · alex@multipliconsult.co.uk

Nick Walton

Director, Walton Wagner · nick@waltonwagner.com

Jay Hodges MRICS

Construction Director, Remian Group · jhodges@remiangroup.com

Jakob Mayer

Project Manager, F/LIST · j.mayer@f-list.at

R E F E R E N C E S

12. Sources and Further Reading

Ellis, R. et al. (2021). A Case Study of a Negotiated Tender within a Small-to-Medium Construction Contractor: Modelling Project Cost Variance. Buildings, 11(6), 260. MDPI. Northumbria University / University of Manchester.

Walton, N. (2026). Practitioner commentary on procurement in prime residential construction. Director, Walton Wagner. Personal communication, April 2026.

Mayer, J. (2026). Outlook: Optimizing Project Value through Integrated Frameworks. Project Manager, F/LIST. Contribution to this report, May 2026.

Constructing Excellence (2011). The Business Case for Lowest Price Tendering? Health Warning. Collaborative Working Champions. constructingexcellence.org.uk

Constructing Excellence (2010). UK Industry Performance Report — KPIs and Benchmarking. constructingexcellence.org.uk

KPMG (2015). Global Construction Survey: Never Done Before. KPMG International.

McKinsey Global Institute (2017). Reinventing Construction: A Route to Higher Productivity. Chapter 4: Cost and Schedule Performance.

National Audit Office (2023). Major Projects Authority: Annual Report. gov.uk

BRCKS (2024). Why 68% of UK Residential Construction Projects Go Over Budget. brcks.io

Cheung, S.O. et al. (2000). Lowest Price or Value? Investigation of UK Construction Clients’ Tender Selection Process. Construction Management and Economics, 18(7). Taylor & Francis.

Designing Buildings (2024). Negotiated Contract; Competitive Tender; Cost Overruns in Construction. designingbuildings.co.uk

Beam Development (2024). Competitive Tender versus Negotiated Contract. beamdevelopment.co.uk

RIBA (2020). How to Choose the Right Construction Contract; RIBA Plan of Work 2020. architecture.com

Planman (2024). Dealing with Cost Overruns — A Guide for UK Architects. planman.app

RICS (2012). Early Contractor Involvement. RICS guidance note, global 1st edition.

University of Minnesota / IPDA / LCI (2015). Motivation and Means: How and Why IPD and Lean Lead to Better Outcomes.

Stanford CIFE (2014). The Impact of IPD on Project Performance: A Comparative Analysis of Case Studies.

BMWSB (2022). Leitfaden Integrierte Projektabwicklung (IPA) für Hochbaumaißnahmen des Bundes.

AIA (2014). Integrated Project Delivery: An Updated Working Definition. AIA California Council.

Project Alliancing Association of Australasia (PAA). Project Alliancing Practitioners’ Guide. alliancing.org.au